The Omnibus on Sustainability Reporting: Where Are We Now?

By Dr. Diana Radovan, Director of Sustainability Policy, Global Electronics Association

Key Summary:

EU Omnibus (2025): Simplifies and delays sustainability reporting under CSRD, CS3D, and the EU Taxonomy to reduce burden while preserving Green Deal goals.

Reporting Delays: “Stop-the-Clock” postpones CSRD for Wave 2 and 3 companies and delays CS3D phase-in; Wave 1 companies receive streamlined ESRS relief for 2025–2026.

Updated Scope & Timeline: Mandatory CSRD reporting starts in 2027 (large EU firms) and 2028 (certain non-EU firms) under simplified ESRS with DMA; SMEs remain voluntary.

CBAM Amendments: Revised CBAM rules adopted in October 2025; final Omnibus measures expected to take effect in 2026.

In February 2025, the European Commission (EC) released its Omnibus on Sustainability Reporting proposal to reduce EU sustainability reporting burden while preserving the Green Deal essence and its impactful sustainability objectives. The proposal addresses both the content („Content proposal”) and implementation timeline (at EU Member State [MS] level: “Stop-the-clock” proposal) of the Corporate Sustainability Reporting Directive (CSRD), Corporate Sustainability Due Diligence Directive (CS3D), and EU Taxonomy (EUT) Directive.

Our Association has consistently advocated for proposed content-related simplification measures regarding sustainability reporting in these 3 key policies. See our position here.

Amendments to the Carbon Border Adjustment Mechanism (CBAM) regulation were also proposed. On 17 October 2025, the Omnibus amendment to the CBAM Regulation was published in the EU Official Journal as Regulation (EU) 2025/2083.

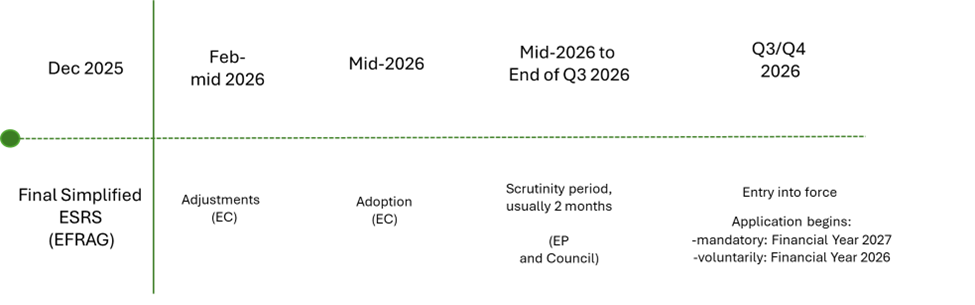

In a parallel process, the European Financial Reporting Advisory Group (EFRAG) has been tasked by the EC with simplifying ESRS, including adjustments to Double Materiality Assessment (DMA) requirements (see expected implementation timelines below).

Abbreviations: EC = European Commission; EFRAG = European Financial Reporting Advisory Group; EP = European Parliament; ESRS = European Sustainability Reporting Standards.

The “Stop-the-Clock” directive (which our Association advocated for) postponed CSRD reporting obligations for Wave 2 and Wave 3 companies (i.e. those that had not already reported under CSRD) and delayed the first phase of CS3D by one year. Wave 1 entities were excluded, prompting the EC to adopt “quick fix” amendments to the European Sustainability Reporting Standards (ESRS) in July 2025, allowing Wave 1 companies to maintain—or, in some cases, reduce—their 2024 reporting scope for 2025 and 2026.

Following months of negotiations, a content agreement was reached by the European Parliament and Council in December 2025 (see our statement here). The content and implementation timeline changes will become legally binding once published in the EU Official Journal (currently expected in March 2026). EU Member States will then have up to 12 months to transpose provisions (exception: CS3D provisions in July 2028). Changes to the CSRD, pending adoption after EU Official Journal publication, are summarized below.

Mandatory 2027 Large undertakings | Mandatory 2028 Non-EU companies | Voluntary SMEs | |

| CSRD scope | Listed and non-listed with: Net turnover >450 m Euro And employees >1000 | Non-EU companies: Net turnover >450 m Euro And subsidiaries or branches with: Net turnover >200 m Euro | Employees <250 |

| Standard | Simplified ESRS, including DMA | Simplified ESRS, including DMA | VSME |

| Assurance | Limited | Limited | None |

Abbreviations: CSRD = Corporate Sustainability Reporting Directive; DMA = Double Materiality Assessment; ESRS = European Sustainability Reporting Standards; SMEs = small, mid- and medium-size entities; VSME = Voluntary Sustainability Reporting Standards. An up-to-date CSRD transposition tracker is available here.

For further information, including changes in CS3D, EU Taxonomy, and CBAM scope, read our upcoming i-connect March issue or contact me at DianaRadovan@electronics.org.